This Time It’s Different

AI valuations are headed for a 50 to 70 percent correction. Scott Galloway called it. Here's why the bubble pops and the technology wins in the same crash.

THE NUMBER: 50–70% — the drop in AI valuations Scott Galloway says is coming inside 24 months. Sounds like the end of the world until you run the arithmetic the other direction. Take 50–70% off OpenAI and Anthropic and you land somewhere around $300–500 billion. That is not a smoking crater. That is where they were priced twelve months ago. The voting machine ran them up a full year’s worth of value in a single year. All Galloway is saying is that the weighing machine wants the year back. The technology keeps compounding the entire time the price is falling. Hold those two facts in the same hand and you have the whole issue.

In The Big Short, the best scene isn’t the casino or the strip club or Margot Robbie in the bathtub explaining subprime. It’s Michael Burry, alone in his office with the lights off and the door locked, watching the housing market keep climbing for two straight years after he’s already bet against it. His investors are screaming. They’re suing him. They think he’s a lunatic who lit their money on fire. And he’s right the whole time. He just isn’t right yet. The famous line he scrawls on the whiteboard isn’t a victory lap. It’s a confession of how lonely the gap is between being correct and being proven correct: “I may be early, but I’m not wrong.”

That gap — between when the fundamentals turn and when the price admits it — is the only thing this whole issue is about.

Scott Galloway is standing in Burry’s office right now. The man called the dot-com crash from a faculty meeting while his colleagues were buying Pets.com, and this week he put a hard number on AI: valuations come down 50% to 70% inside two years. Every doomscroller on X grabbed the number and started dancing on the grave of the technology. They grabbed the wrong half of what he said. Because Galloway is not arguing that AI is fake. He’s arguing that the price is early. Those are not the same claim, and the distance between them is where you either make money or lose it over the next two years.

⚖️ The Only Framework That Matters Here

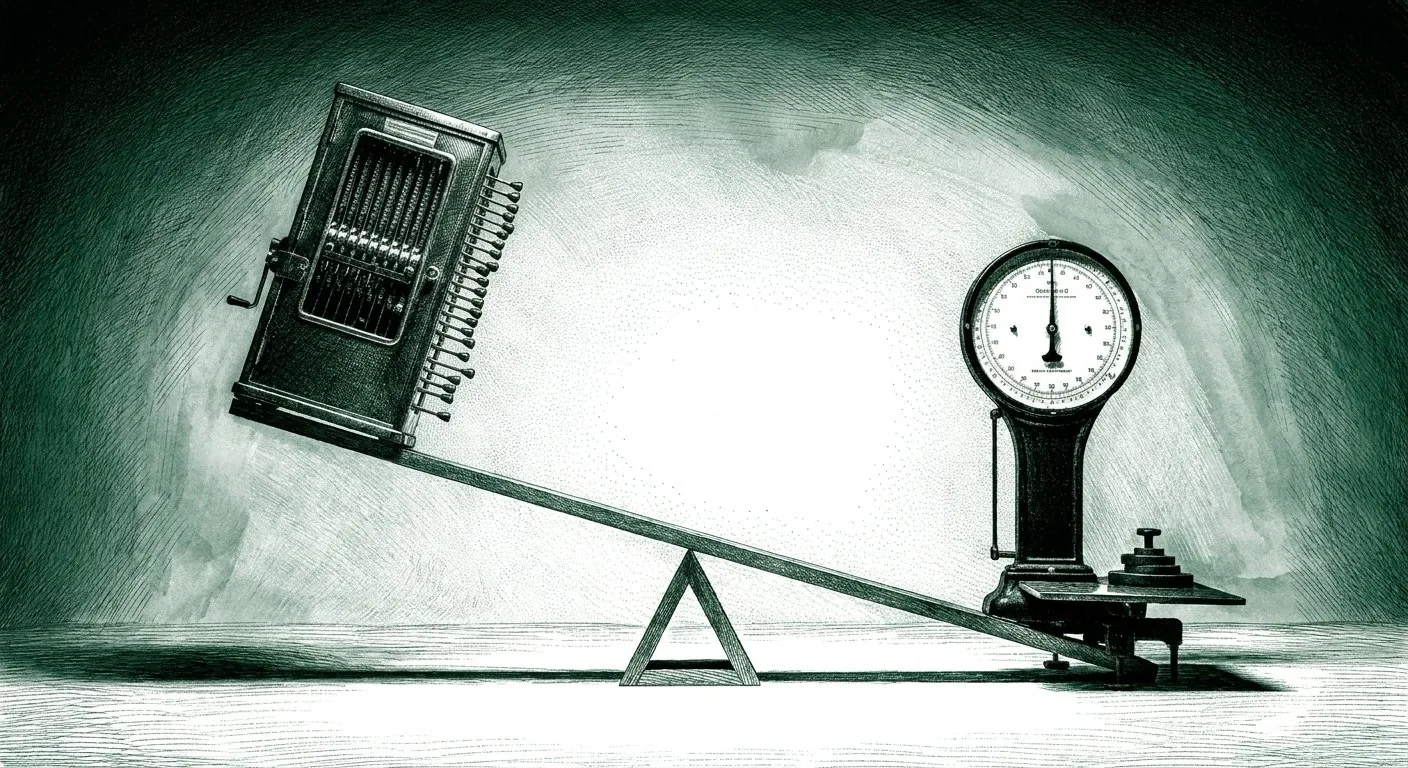

Ben Graham gave us the tool sixty years ago, and Warren Buffett has spent his entire career quoting it because nothing better has ever been built. In the short run, the market is a voting machine. In the long run, it is a weighing machine.

Sit with how precise that is. In the short run, price is a popularity contest. It’s a tally of how many people want in, how loud the momentum is, how good the story sounds at the dinner party. Votes are emotional, they’re fast, and they have nothing to do with what a thing is actually worth. Then the long run arrives, and the machine changes. It stops counting hands and starts measuring mass. Cash flow. Margins. The boring arithmetic of what a business actually throws off. And the weighing machine has never once, in the entire history of markets, lost to the voting machine. It just takes its time.

Venture capital is the purest voting machine ever constructed. It is a momentum business by design — when a company is working, there is no price too high, because the only thing that matters in the short run is owning the thing everyone else is about to want. That’s not a criticism. That’s the job. And the voting machine did exactly what it does: it ran Anthropic from roughly $300 billion to a trillion dollars in twelve months. It carried OpenAI to the same neighborhood. It is about to walk SpaceX, OpenAI, and Anthropic through the IPO door at a combined value north of $3.5 trillion, none of them profitable.

That was the vote. Now the weighing machine clocks in. And what it’s about to weigh is uncomfortable.

The strategic read: Stop arguing about whether AI is real — that’s a settled question and it’s the wrong one. The live question is whether the price is real, and price is a separate machine running on a separate clock. Every dollar you have in this game should be sorted by which machine you’re betting on and what time horizon you can survive.

🧮 What the Weighing Machine Actually Weighs

Here’s the math nobody wants to put next to the scary number, so we will.

Anthropic does about $47 billion in run-rate revenue. Real revenue — not vapor — but not a dime of real free cash flow yet. Now price it. At a trillion dollars, you’re paying roughly 21 times revenue for a company that doesn’t yet generate cash.

Be the buyer at that trillion-dollar mark for a second. To make a venture-style return, you need this thing to double — you need it to become a two-trillion-dollar company. Fine. What does a two-trillion-dollar company have to produce? At a mature software multiple of 20 times free cash flow, two trillion in market value means $100 billion in annual free cash flow. And to throw off $100 billion in cash at a genuinely fat 25% free-cash-flow margin, you need $400 billion in revenue. That’s roughly eight times what Anthropic does today. You are underwriting an 8x revenue ramp on a company already running at a $47 billion clip, just to double your money. That is a brutal bet. Possible — this is the most explosive technology any of us has ever watched — but brutal.

Now stand in the other guy’s shoes. The investor who bought a year ago at $300 billion. He needs the same double, to $600 billion. Same 20x cash flow gets him to $30 billion in free cash flow, which at the same 25% margin means about $120 billion in revenue. That’s about two-and-a-half times today’s run rate. In a market growing the way this one is, 2.5x over a few years isn’t a prayer. It’s a base case.

Same company. Same models. Same week, even. The only variable that changed between those two investors is the price each one has to justify — a 2.5x story versus an 8x story. That gap, and nothing else, is what a “correction” actually is. The fundamentals decoupled from the basics of the business. Galloway’s 50–70% is just the weighing machine pulling those two lines back together.

The strategic read: Before you buy a single share of anything AI, do this one piece of arithmetic — what revenue ramp does today’s price force me to believe? If the honest answer is 8x, you’re voting. If it’s 2.5x, you’re weighing. Underwrite like the early buyer or don’t underwrite at all.

🌷 Every Bubble Is Air. This One Has an Engine.

Here’s where we get off Galloway’s bus, or at least move to the back of it.

Pull up the lineage of manias and you can see the shape of human nature repeating: tulip bulbs in 1637, the South Sea and Mississippi schemes in 1720, railway mania in the 1840s, the run-up to 1929, the Nifty Fifty, Japan’s everything-bubble in the late ’80s, dot-com in 2000, housing in 2008, and the whole crypto-NFT-meme-stock circus of the last decade. Each one bigger than the last. And AI dwarfs every single one of them on speed — it came further, faster, than any run-up in the recorded history of markets.

But here’s the thing that keeps us out of the doomer camp, and it’s the most important sentence in this issue: every prior mania was mostly air. A tulip is a flower. A Bored Ape is a JPEG. Pets.com was dog food sold at a loss with a sock puppet for a CMO. When the weighing machine showed up for those, there was nothing underneath — so the price didn’t correct, it evaporated.

AI is the first mania in history with an actual industrial revolution sitting under the froth. That’s precisely why it ran further and faster than tulips ever could — because underneath the speculative insanity, the thing actually works, and it’s getting better every quarter. Coding is already permanently changed. So the weighing machine does something different this time: it reprices the stock without repealing the technology. The dot-com crash is the model. It vaporized Pets.com and Webvan and pets-dot-whatever — and in the very same downturn, it minted Amazon and Google. The internet didn’t die in 2001. Its price got right, and the real businesses walked out of the rubble worth more than ever.

That’s the correction coming for AI. Not an extinction. A sorting.

The strategic read: “We’ve seen this movie before” cuts both ways, and most people only watch half of it. The bubble pops and the technology wins — at the same time, in the same crash. Your job isn’t to call the top. It’s to be holding the Amazon, not the Pets.com, when the weighing machine finishes its count.

🪑 The Correction and the Cost Collapse Are the Same Event

Here’s the part almost nobody is connecting, and it’s the one that actually tells you who gets hurt.

An equity correction and an inference-cost collapse are the same event read from two different chairs.

Watch what’s happening to the price of intelligence right now, in real time. Lindy just moved 100% of its traffic off Anthropic’s models onto China’s DeepSeek v4 — and reported it came out both cheaper and better on its core jobs. Fireworks and Harvey published a result where a small open-weight worker model (GLM-5.1) that calls a frontier model (Opus) only when it absolutely needs to beats the frontier model running solo — 18 versus 14 passing tasks — at 39% of the cost. Gary Marcus, watching the same tape, flagged a report that even Sam Altman has warned of a severe, first-of-its-kind pullback in AI spending, and called it what it is: “death of tokenmaxxing… a very serious issue for all three big IPOs.”

Now connect it. If the price of inference is collapsing — and it is, fast — then the company that suffers most is the one selling expensive inference. That’s the US frontier labs. The exact companies trying to IPO at a combined $3.5 trillion are the ones whose core product is getting commoditized underneath them while the prospectus is still at the printer. The equity has to weigh that. The same force that lets a startup cut its model bill by 60% is the force that compresses the seller’s multiple. One event. Two chairs. The deployer cheers; the lab bleeds.

And the beneficiaries aren’t only Chinese. They’re the open-weight tier broadly, and — this is the underrated one — they’re the perfectly good US models that were state of the art six months ago and now run cheap. You do not need the frontier for most work. You need it for the hard 10% and a cheap, fast, good-enough model for the other 90%. The whole market is figuring that out at once.

The strategic read: Find out which chair you’re in before the market sits you down in it. If your business sells premium tokens, the cost collapse is your correction. If your business buys tokens, it’s the best margin tailwind you’ll get this decade. Route the cheap model under the expensive one starting today — frontier for the hard problems, good-enough for the rest.

🍎 The Sleeper Who Wins the On-Device Round

If intelligence is getting cheap enough to run on the machine in front of you, then the toll booth moves. It comes off the cloud and lands on the device. And the company that owns the device has been sitting there the whole time, written off because its chatbot stinks.

Google’s Gemma 4 12B now runs on a 16GB MacBook. Sit with that. A genuinely capable model, from a frontier lab, running locally on consumer Apple silicon, no cloud bill, no data leaving the machine. One tweet on it did 680,000 views with a four-word thesis attached: “cloud is not the endgame.” The Deep View got Apple’s Mac hardware product manager, Doug Brooks, on the record this morning, and the picture he paints is a company that quietly built exactly the right hardware for this moment — unified memory, the Neural Engine, power efficiency — years before anyone needed it. The receipts: Mac mini backorders pushed out four to five months. Ninety percent of the staff at frontier labs run Macs. And the labs now ship their desktop apps Mac-first — Claude Cowork, Codex, Perplexity, the Gemini desktop app — Windows comes later.

Everyone spent two years dunking on Siri and missed that Apple became the landlord of on-device AI without saying a word about it. The Siri narrative was the misdirection. The silicon was the play.

The strategic read: When the model shrinks to fit the device, value migrates from whoever rents you compute to whoever sold you the hardware. If you’re hunting the AI names that benefit from the cost collapse instead of bleeding from it, start with the one whose logo is on the laptop.

🎓 “No ROI” Is Tuition — and Read Dara Correctly

The bear’s heaviest club is the ROI gap. Bain put out a survey this week with a brutal one-liner: “The technology worked. The value didn’t arrive.” Deployments run exactly as designed; the modeled cost savings just aren’t landing on the income statement on schedule. An MIT figure floating around says 95% of AI projects connect to no return a CFO can name. Galloway swings that 95% like a hammer.

We’ve been calling this tuition since I Drink Your Milkshake (Sam Altman’s own “J-curve lull,” May 4) and we built the whole Emmet’s Roof issue around it (May 21). Here’s the mechanism. Companies get AI-pilled, hand the same tool and the same budget to every single employee, and say go forth. Of course there’s no clean ROI yet — they’re paying tuition to get the systems wired and the people ramped. The return doesn’t show up evenly across the workforce. It shows up after the 100X operators get cranked up and the 1X drag gets moved out. The math we ran in May still holds: the top performer using these tools didn’t go from 10 to 11. She went from 10 to 100. The gap that used to be 9 points is now 98. That gap is invisible on a quarterly income statement and then, all at once, it isn’t.

Which brings us to the quote everyone is misreading. Uber’s Dara Khosrowshahi told investors the company “blew through our AI budget in a quarter, for the whole year.” The doom crowd quoted it as proof AI is too expensive. Read what he actually said next: “We’re going to meter headcount increases.” He is not cutting AI. He is curtailing hiring to pay for AI. That is the single most bullish sentence in the entire story, and it’s wearing a cost-complaint costume. When a CEO chooses to freeze human headcount in order to fund the machines, the machine just won a budget fight against payroll. That’s not the sound of a bubble bursting. That’s the sound of substitution beginning.

The strategic read: A pilot that runs as designed but misses its cost-savings target is not a failed pilot — it’s tuition paid and a base to build on. Reframe the value case (revenue, quality, throughput) before your finance team scores it against the original headcount model and kills the second round of funding.

🚪 The Window, the Lockup, and the Buyer of Last Resort

So if the smart money knows the weighing machine is coming, why the frantic rush to go public right now? You just answered your own question.

The dash through the IPO window is the voting machine trying to print one last tally before the recount. Galloway put it about as bluntly as it can be put: when these companies go public, it’s effectively the smartest people in the room saying we’ve squeezed as much out of this as we can, now we need to find someone to sell to at this price. The public is the buyer of last resort. That’s not cynicism, it’s sequencing — the people who know these companies best are the first sellers, and retail is the last.

And the trigger that turns Galloway’s prediction from a thesis into tape isn’t priced in yet: the lockup. Insiders and employees can’t dump on day one. But when the lockups roll off — 90, 180 days out — the people who rode this from $300 billion to a trillion get their first chance to lock in a generational gain, and a lot of them will take it at once. That’s the mechanical event. Watch the lockup calendar more closely than the IPO pop.

🏰 Build the Fort, Not the Forecast

The correction is inevitable. The date is not. Anyone who tells you they know the timing is selling something — Burry was early by two years and nearly got fired for it. So the move isn’t to time the market. The move is to build a balance sheet that doesn’t care when the recount lands.

Look at what the patient money is actually doing. Warren Buffett — the man who has quoted the weighing machine line his whole life — just put $10 billion into Alphabet, part of an $80 billion raise. He bought the toll booth, the picks-and-shovels, the company that owns its own silicon and prints cash today. He did it the same week Galloway said sell the cars. Both can be right. You can believe the application-layer equities are due for a 50–70% haircut and that the infrastructure underneath compounds. We made the same call on June 1: own the toll, fade the racer.

So here’s the playbook. Own the toll where you can. Run your inference cheap — frontier for the hard 10%, good-enough for the rest. Keep dry powder, because the best assets of the next decade are about to go on sale to whoever has cash when the over-leveraged get marked down. Underwrite every position like the man who bought at $300 billion, never like the one who paid a trillion. When the weighing machine finishes its count, you don’t want to be the buyer of last resort. You want to be the buyer everyone else has to come to.

So no — this time isn’t different. The technology is. The price never is.

📊 The Daily 5

🦞 Anthropic beats OpenAI to the IPO line, and hands Wall Street a $3.5 trillion problem. The first pure-play lab filed near $960 billion. Stack SpaceX and OpenAI behind it and you’ve got the biggest liquidity stress test in decades, with not one of the three turning a profit. The window is open. The question is who’s left holding it when it shuts.

🍎 Apple wins the round nobody was watching. Gemma 4 12B runs on a 16GB MacBook; Apple’s Mac hardware chief tells The Deep View that mini backorders run four to five months and 90% of frontier-lab staff are on Macs. When the model moves on-device, the landlord is in Cupertino.

🐉 The cost collapse has a country. Lindy churned 100% to DeepSeek v4 and got cheaper and better. A GLM worker calling Opus only when needed beats Opus solo at 39% of the cost. Galloway’s prediction of a flight to cheap models isn’t 90 days out — it’s already on the tape.

📉 Bain: the AI worked, the savings didn’t show up. Deployments run as designed; the modeled cost savings aren’t hitting the income statement on schedule. That’s a forecasting failure, not a tech failure — tuition, not a tombstone. The teams that get round-two budget reframe the win before finance scores the loss.

🏛️ Bernie Sanders wants the public to own half the labs. His bill would tax 50% of OpenAI, Anthropic, and xAI equity into a public wealth fund with board seats. It won’t pass. That a senator can say it out loud and not get laughed off the floor is the actual story — the mood is turning while the valuations are still peaking.

Sources

- Scott Galloway: 95% of enterprise AI spend connects to no return a CFO can name — The AI Corner (Prof G Markets breakdown)

- Quote origin: “voting machine / weighing machine” — Graham via Buffett — Quote Investigator

- $960 Billion: Anthropic Beats OpenAI to the IPO Filing — 24/7 Wall St.

- Can Wall Street Absorb $3.5 Trillion in New IPOs? — 24/7 Wall St.

- Dara Khosrowshahi on Uber’s AI spend — via @patrick_oshag

- Lindy switches 100% of traffic to DeepSeek v4 — @matthartman quoting @Altimor

- GLM-5.1 worker + Opus advisor beats Opus solo at 39% of cost — @sgurumur (Fireworks × Harvey)

- Gemma 4 12B runs on a 16GB MacBook — @kanikabk

- Gary Marcus: death of tokenmaxxing — @GaryMarcus

- How Apple silicon keeps quietly piling up AI wins — The Deep View (Doug Brooks interview)

- Bain survey: AI delivers less cost reduction than firms predicted — Bloomberg, via The AI Brief

- Bernie Sanders’ American AI Sovereign Wealth Fund Act — via CO/AI (June 4) and Aligned News policy feed

More like this

Ignorance Is Bliss

The state moved on AI this week — a toothless order on top, a populist revolt underneath. Everyone wants the steak. Nobody wants to watch the cow get butchered.

The Meter’s Running

Subsidized intelligence is over. The meter that finally priced the machine is turning toward the seat next to it.

Someone Made Fire

Anthropic filed the first big pure-play AI IPO this week. But the model is the lotion, not the cure. What they're really taking public is the operation.